Watch the video

Quick version? Watch the video. For full context, read the article.

When a software builder mentions they "also have their own app", the reflex is often: nice hobby project. I get the reflex. But once you know the numbers, the verdict flips. Actually getting an app into both stores — working, multilingual, with a payment model, and maintained year after year — is no hobby. It's a rare speedrun through three filters that each, on their own, wipe out the majority.

Filter 1: getting through the gate

Submitting an app is no formality. In 2024 Apple rejected roughly one in four submissions — 1.93 million of 7.77 million — and terminated more than 146,000 developer accounts (Apple App Store Transparency Report 2024). That same year Google blocked more than 2.3 million apps that violated policy (Google via BleepingComputer, 2024).

And that's per platform. Anyone who wants to be in both stores faces App Review (review time, rejects, annual SDK requirements) plus Google Play's target-API requirements and the new identity verification — two independent bureaucracies, each with its own rejection rules.

Filter 2: staying alive

The second filter is coarse. In early 2023, 34% of all apps had gone more than two years without an update (30% App Store, 37% Google Play) — Apple's own definition of "abandoned" (Appfigures, 2023). The stores actively purge those dead apps: Apple removed 540,000+ abandoned apps in a single quarter (AppleInsider, 2022), and Google Play shrank in one year from ~3.4 million to ~1.8 million apps — nearly half gone (9to5Google, 2025).

So "keeps working and maintained" is demonstrably the exception, not the norm.

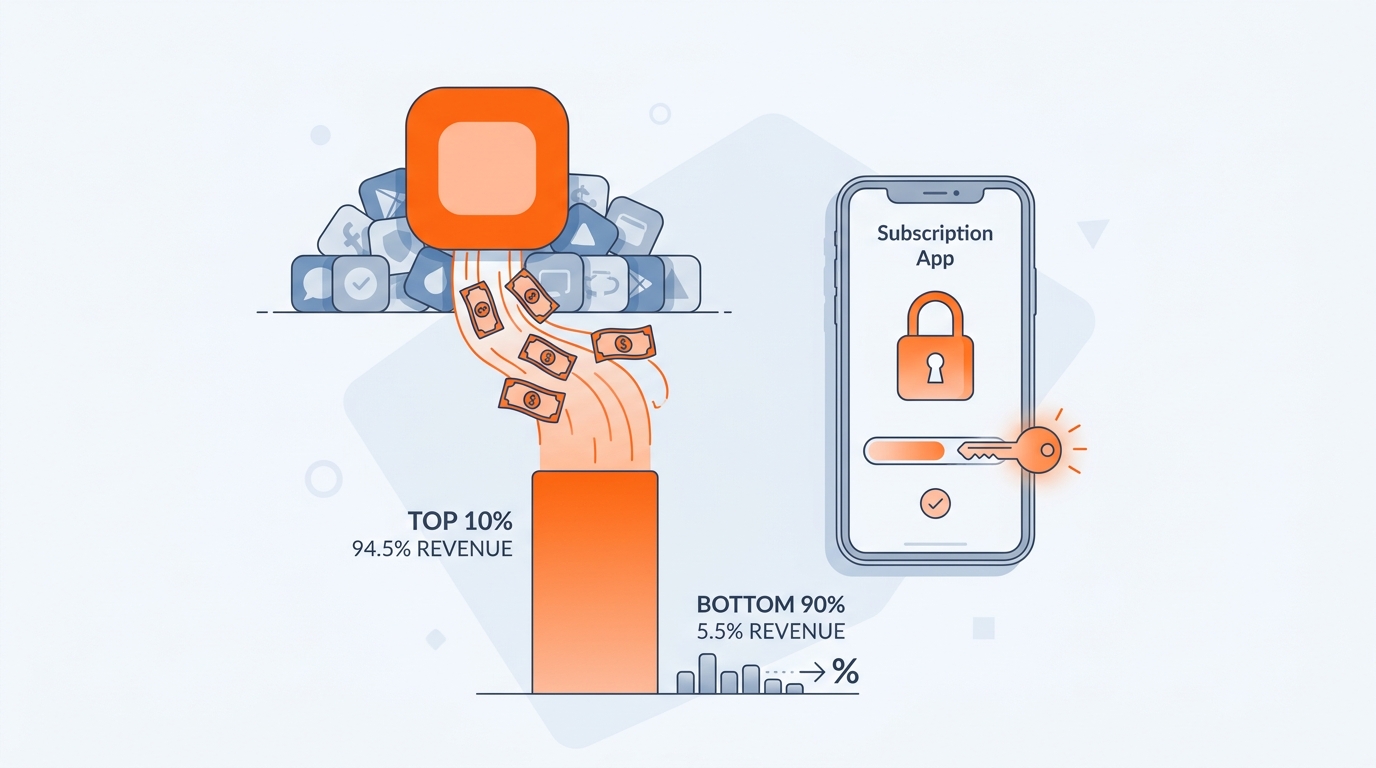

Filter 3: earning anything from it

The third filter is the sharpest. Of new subscription apps, only 17.3% reach $1,000 MRR within two years, and just 4.6% reach $10,000 (RevenueCat, State of Subscription Apps). Revenue is extremely concentrated: the top 10% of apps take ~94.5% of all subscription revenue. Building a payment model that clears Apple's and Google's receipt verification is a project in itself.

What clearing it actually proves

Stack the filters. A product that gets through App Review and Google Play, stays maintained after launch, runs in multiple languages and has a working payment model has passed three filters that each, individually, kill the majority. That's no loose hobby project — it's proof of shipping capability: the ability to take an idea through the whole chain, from concept to deployment, payments, maintenance and ongoing development.

And that's exactly what most "it works on my laptop" projects never reach. The difference between a demo and a running product is rarely in the clever core; it's in the boring, hard last 90%: review, payments, encryption, multilingual support, maintenance.

That's also why I build and run my own products. Dreamalizing is going through exactly this gauntlet right now: web live, iOS via TestFlight (beta), a payment model and 14 languages, Android on the way. Not because a dream app is my core business, but because it proves I get AI products through the chain — the same discipline I apply in client work around AI in production.

An app in both stores isn't a hobby. It's the opposite: proof that you finish what you start.

An honest caveat: there's no reliable public figure for the exact share of developers who reach both the App Store and Play Store. The rarity above is substantiated via the individual filters — review rejection, abandonment and the revenue tail — not via a single count. And RevenueCat only measures apps that already built a payment model, so the real base rate of "earns anything" across all apps is likely lower still.